What If Everything You Know About Money Is a Lie? There are certain secrets in this world that no one tells you. Or maybe it’s just that the system is built in a way to make sure they never reach you. Today, I’m going to talk about one such truth, the reality of money.

When you press a few keys on your keyboard and log in to your bank account, you see a bunch of numbers. We call that your bank balance. But here’s the thing, those aren’t actually money. They’re just numbers. Now why do I say that? You’ll need to dig a little deeper to really get it.

What Is Money, Really? (Shadow Banking System)

Banks have to create this illusion, because that’s their job. The money you see in your account, the digits on the screen, they only exist in the system. In reality, banks don’t have that much physical cash lying around.

Now if you're thinking just about your own account, you’re missing the bigger picture. You might say, "But whenever I go to the bank and ask for money, they never say no." Sure, but imagine a bank with 100 account holders, and all of them show up to withdraw their money at the same time. What do you think would happen? The bank would probably collapse. And yes, bank failures like that have happened before. You’ve probably heard of a few.

So the question is, what exactly are banks doing behind the scenes that makes me call your account balance just a bunch of numbers?

Phantom Liquidity: The Money That Doesn’t Exist

Let’s say you work for a company, and every month you get a salary. What’s really happening there? The company’s bank account is debited, and your account is credited. But no actual cash changes hands. Just numbers are moved around. It’s all just an entry in the system, a record.

Put simply, your bank balance is an illusion. You see it, but it isn’t real. You can’t touch it. The idea of money in your account creates a sense of wealth, but it has no physical form.

This is what’s called phantom liquidity.

Now when a bank gives out loans to others, it’s actually lending your money to someone else. But the mechanism isn’t that straightforward.

Fractional Reserve Banking: The Legal Illusion

Here’s what really happens, suppose a bank has deposits worth ₹100 crore. Out of that, it keeps a small portion, say ₹4–5 crore, in cash. The rest is lent out. This system is called fractional reserve banking. It means banks don’t have to keep your full deposit as cash. They’re only required to keep a small percentage in reserve. The rest can be used to issue loans.

So if you deposit ₹10,000 in a bank, it might keep ₹1,000 in reserve and lend out ₹9,000 to someone else. That person then deposits the ₹9,000 in another bank. That second bank keeps ₹900 and lends out ₹8,100. This cycle keeps going.

What ends up happening is — that original ₹10,000 deposit multiplies through the system and turns into ₹70,000 or ₹80,000 worth of digital money.

This is called credit creation. And this is the core secret of the banking system, new money is created, even though no new physical currency is printed.

So when you look at your account balance, it doesn’t mean that money physically exists. It exists because the system assumes it does because the system runs on trust. And it works, as long as people don’t all try to withdraw their money at once.

But if they do? The system crashes. That’s called a bank run. And no, that’s not just theory, it's happened multiple times in history.

2008 Financial Crisis: The Day Trust Collapsed

Now let’s talk about 2008.

What happened in 2008 wasn’t just a recession. It was a global shock. A fuse blew in the system of trust that underpins the economy.

So what really went down?

It started with the US housing market, somewhere in the early 2000s. There was this idea floating around — owning a house meant you were successful. So the number of people buying homes skyrocketed.

Banks in the US began giving out home loans at an aggressive scale. Now you might say, "So what? That’s normal." But here’s the twist — they were giving loans to anyone. Even people with bad credit scores, unstable jobs, or no reliable income. These were called subprime mortgage loans — loans given to high-risk borrowers.

Banks figured, "People always repay home loans. And even if they don’t, we’ll just sell the loan to someone else."

Most banks knew these borrowers wouldn’t repay. But they didn’t care. They came up with a trick, they bundled these risky loans together and turned them into bonds. Basically, they packaged them and created what’s called Mortgage-Backed Securities (MBS).

How does that work?

Let’s say the bank has 100 home loans. It bundles the expected monthly payments from all those loans into a financial product. That product, an MBS — promises steady income for the next 20 years. And then the bank sells it to investors.

Who buys them?

Big investors — mutual funds, pension funds, hedge funds. Why? Because these products seemed to offer predictable, monthly returns.

And here’s the kicker, these MBS were sold not just in the US, but around the world. India, Europe, Japan — everywhere. Because the credit rating agencies gave them “AAA” ratings, calling them ultra-safe. But that safety was just on paper. The reality was something else entirely.

Here’s the translated and proofread version of your text in natural, clear English while keeping the original tone and flow:

So where did things go wrong?

Because loans were handed out on such a massive scale, a huge bubble formed within the system. People started buying homes, prices began to rise, more people rushed to buy, and prices kept climbing. Property values shot up. But eventually, homes became far too expensive, and many people simply couldn’t repay their loans. Why? Because their repayment capacity hadn't changed.

A point came where people just stopped paying.

And that’s when things slowly began to collapse.

It was like a domino effect. Those who couldn’t repay had their homes foreclosed. Suddenly, the market was flooded with houses for sale, which drove prices down. As a result, people looked at their situation and said, “My home is now worth less than the loan I took for it.” And some of them intentionally stopped paying.

When people stopped paying their loans, the money flowing into MBS (Mortgage-Backed Securities) also stopped. That meant the investors, banks, investment firms, insurance companies stopped getting paid.

MBS turned into terrible investments almost overnight. On paper, banks and investment firms still had those assets, but in reality, their balance sheets were filled with worthless digital numbers.

These financial products were so tangled up with each other that no one could really figure out where the risk was or how big it was or how to unwind it.

Since the loans weren’t being repaid, MBS were no longer assets, they became liabilities.

And the biggest blow hit an investment bank called Lehman Brothers.

September 15, 2008 – Lehman Brothers collapsed. And that day, the global economy had a heart attack.

Lehman Brothers was a 150-year-old investment bank. They had poured massive amounts of money into MBS.

They were operating at a 45:1 leverage ratio. meaning for every $1 they had, they had borrowed $45.

In simple terms, most of what they showed on their balance sheet was a mirage, profit only on paper.

On September 15, the bank filed for bankruptcy. No one stepped in to buy them out. The government didn’t rescue them either.

That day, people realized something that bank balances are just numbers. Nothing more.

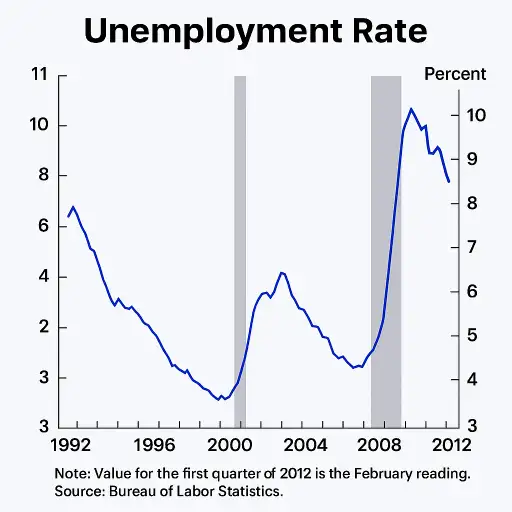

Trust in banks evaporated. Stock markets crashed. Companies started firing people. Banks froze lending.

Millions around the world lost their jobs. Many lost their homes. Some took their own lives.

And that’s what triggered the recession. unemployment, slowdown, economic instability.

Why did this crash happen?

Because the system was sitting on a bubble. And that bubble was called blind trust.

Banks believed, “We’re too big to fail the government will save us.”

Regulators thought, “The market will correct itself.”

And the average person thought, “Buying a house is always a smart investment.”

But reality was different.

Banks cheated, rating agencies backed them, the government looked the other way and the common man paid the price.

And this wasn’t just America’s story. Countries like India felt the shockwaves too in IT, real estate, across the entire economy.

Why This Still Matters Today

As long as there’s trust in the system, those digital numbers work.

But the moment trust breaks the numbers fall apart.

2008 wasn’t just a year it was a warning.

That no matter how digital, no matter how sophisticated the system looks… it's not permanent.

When you deposit money in a bank, you feel like it’s safe there. But is it really?

The truth is it’s just digital numbers on a screen.

Banks don’t actually keep all that money. They lend most of it out.

And the entire banking system?

It runs purely on trust.